In order to avoid unwanted changes of social security (soc.sec.) systems with the consequences that pension entitlements could arise in more countries, entitlement to unemployment money could cease in a country, etc. it is highly recommended to assess consequences on social security before starting an activity in another state.

The following article should give a rough overview of the general rules for coordination of social security for multi-state workers/self-employed people:

Within the EU/EEA/Switzerland soc.sec. responsibility is determined by Reg. (EC) 883/2004. A person can only be subject to social security in one state. By this regulation the employee should be protected from multiple insurance in case of multi-state work.

Basically, a person who is carrying out his or her (self-)employment in one state is subject to soc.sec.in that same state (principle of territoriality).

Exception from principle of territoriality

An exception of that principle applies in case of secondments from one country to another country. The social security responsibility can remain in the home state of the person up to 24 months. Self-employed persons can apply this exception as well, as long as the activity carried out in the other state is similar or identical to the activity usually carried out in the home state.

If a secondment is planned for more than 24 months then there would be the possibility to apply for an exceptional agreement for further being covered by the soc.sec. in the home state. The two involved states coordinate and take a decision on the competent state.

A1 certificate

In order to be able to prove the social security competence of the other state it is to be recommended that all employees carrying out their work abroad hold form A1 always with them. A1 form has to be applied in the country whose regulations for social security purposes are relevant.

Moreover, there are special rules for employees who are physically performing their work in more than one country at the same time:

One employer – physical presence (work performed) in more than 1 country

Social security responsibility is based on the physical presence in the home state of the employee.

- Activity of > 25 % in home state (eg.home office) -> coverage by soc.sec. of home state

The foreign employer then has to register in the home state for social security purposes and to pay the soc.sec. contributions to health insurance fund in the home state.

- If substantial home office activity (> 25 %) is only caused by COVID-19 -> this triggers no shift of soc.sec. responsibility into home state if the only reason for home office was COVID-19.

- Activity is exercised for < 25 % in home state, the employer state is responsible for social security.

Two or more employers – physical presence (work performed) in more than 1 country

- Total work (from all activities) is substantially (> 25 %) exercised in the home state or

- if < 25 % is exercised in home state but employers are in different countries

- employee is covered by soc.sec. in home state.

All employers in other EU/EEA/CH states have therefore to register in home state of employee and to collect social security contributions from each employment separately up to the maximum base for contribution calculation (=EUR 5.550 in 2021). If in total (that means with all employment relationships together) the maximum contribution base is exceeded, then the employee may apply for a refund of the amount exceeding the maximum contribution base after the end of the year.

Self-employment in two or more states

Activity > 25 % in home country -> soc.sec. responsibility of home country

Activity < 25 % in home country -> soc.sec. in that state where center of activity or main activity is carried out.

Self-employment and dependent work in two or more (different) states

In any case soc.sec. obligation is in that state where dependent work is exercised.

Work performance outside of EU/EEA or Switzerland

Basically the principle of territoriality is applicable in this case, ie soc.sec. regulations of that state are applied where work is performed. It is to be assessed by the individual national system of soc.sec whether there is an insurance obligation. If, according to each national law, insurance obligation is given in both states, this could result in double charging for social security contributions in two states.

Nevertheless, between many states there are bilateral agreements which coordinate in which state the employee should be covered by social security. Hence, bilateral agreements can prevent from double charging of soc.sec. contributions in two states.

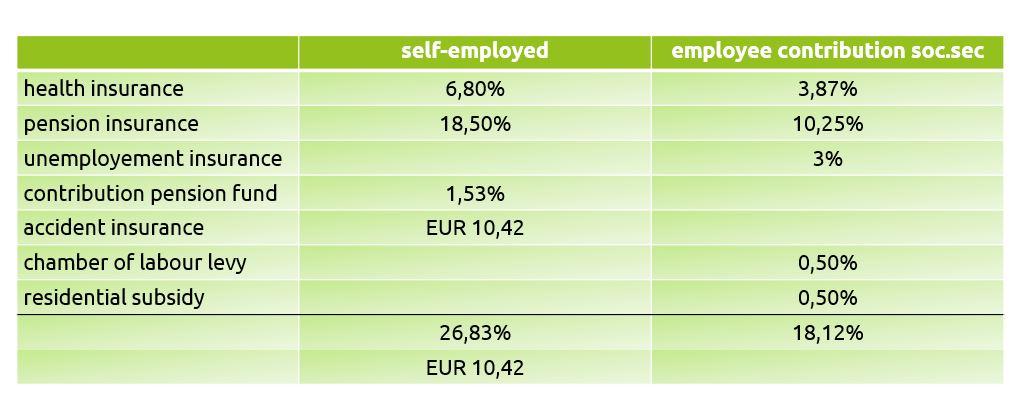

In Austria soc.sec. consists of the following (payable per month based on gross income):

As a result, please make sure to clarify any potential effects on social security or taxation upfront with your employer. ARTUS tax consulting (E: info@artus.at, T: +43 1 5137900-0) will also be happy to support in case of any questions you may have.

PS: Please note, that we are no native speakers and that our blogposts were translated with the help of google translate.